How to Find & Select a Financial Advisor: The Complete Guide

Selecting a financial advisor isn’t a luxury—it’s a necessity in many cases. Unfortunately, only 27% of Americans have a current financial advisor (YouGov, 2024), considering the increasing need for expert planning. Given that the financial advisory services market will also expand to reach a value of $94.41 billion by the year 2029 (Mordor Intelligence, 2024), it is understandable why people understand that they need personal advice.

There is over 50 trillion dollars expected to change hands between Baby Boomers and the younger adults, and with an expected growth of financial advisor jobs by 17 percent between 2023 and 2033 (Bureau of Labor Statistics), the world of finance is shifting rapidly. With investments and retirement, estate planning, and taxes, there seems to be a lot to deal with in the current financial decisions without the help of a professional.

This advice in steps will help you find an answer on how to find a financial advisor that meets your needs and what to consider when choosing a financial advisor to help you achieve your financial prosperity over a long period.

Why You Might Need a Financial Advisor

Money management, earning money, saving money, and investing money may seem fairly straightforward, but life is often unpredictable. You may be going through new heights, responding to economic adjustments, or even ahead of the art towards the future, and in a few instances, financial assistance can work wonders. The reasons as to why you may consider hiring a financial advisor are many, including one-to-one investment counseling to tax planning, and estate management.

Beyond portfolio returns, the benefits of a financial advisor include comfort, professional advice, and a strictly disciplined trajectory to long-term accretion. Financial decisions are getting even more entangled, and many Americans are turning to professionals to help them. As a matter of fact, 35 percent of them use financial advisory services, more so during transition.

Major Life Events That Need Financial Planning

Some life events confirm that doing things on one’s own isn’t always the best idea. Industry statistics show that the first-time consultation age with a financial advisor is 33, coinciding with critical financial milestones. These life events for financial planning usually indicate it’s time for professional advice:

- Marriage and merging finances

- Having kids and paying for education costs

- Inheriting wealth or unexpected wealth

- Beginning a new business or a new career

- Divorce and asset partitioning

- Planning for retirement or retirement from the workplace

These are situations that frequently demand sophisticated decision-making, and a financial counselor can assist you in making decisions that meet both immediate and future objectives.

Sophistication of Personal Finances Today

From cryptocurrencies to international markets, sophisticated financial planning is the new standard. Financial advisors handled more than $62.62 trillion in assets alone in 2024, highlighting the scope and complexity of investment choices.

Contemporary services extend well beyond conventional stock selection. Advisors today help with:

- Investment guidance and rebalancing

- Tax-effective planning and loss harvesting

- Legacy and estate planning strategies

- Managing multiple retirement income sources

- Dealing with cryptocurrency and alternative investments

Furthermore, 60% of financial advisors are confident that AI-based tools will further improve decision-making, highlighting how technology is transforming the industry of personal finance.

The Confidence and Expertise Gap

Though DIY investing websites have opened the doors to financial markets, a lot of people ultimately reach their limit. With market fluctuation or unfamiliar tax regulations, investment confidence can disintegrate. The DIY investing versus financial advisor showdown hinges on time, intelligence, and emotional control.

You might benefit from guidance if:

- You feel burdened by handling finances on your own

- Make spontaneous choices with market fluctuations

- Have a hard time being consistent because of a hectic schedule

- Don’t have a basic financial education

- Fall prey to behavioral finance mistakes

Having a trusted advisor fills you in on this gap—providing you with clarity, strategy, and confidence along the way.

Types of Financial Advisors Explained

Not every financial advisor works the same way—or for the same kind of client. Knowing the different kinds of financial advisers is vital when figuring out who to entrust your cash to. The best adviser for one individual can be entirely unsuitable for another, based on goals, price, and complexity of need. The type of compensation the adviser receives, the level of professional duty to clients, and whether human or computer power fuels their services are some of the main differences.

Fee-Only vs Commission-Based vs Fee-Based Advisors

Deciding how you want to pay for advice is one of the earliest choices to make. It affects both the quality of advice and possible conflicts of interest. Here’s a summary of the most popular models:

| Type | How They’re Paid | Pros | Cons |

| Fee-Only | Flat fees, hourly fees, or a percentage of assets | Transparent, less conflict of interest | May seem costly at first |

| Commission-Based | Paid by third parties (such as mutual funds, insurance) | Lower or no out-of-pocket expenses at the onset | Risk of biased product suggestions |

| Fee-Based | A hybrid of fees and commissions | Some flexibility may provide a wide array of services | Potential for conflicts and less transparency |

As of 2024, 60% of financial advisors are employed by private companies, and the median yearly salary is $102,140 (Bureau of Labor Statistics). When shopping around, always request a clear explanation of how the advisor gets paid and what that will cost you.

Fiduciary vs Suitability Standard

One of the greatest contrasts in the world of advising is between fiduciary vs non-fiduciary advisors. A fiduciary financial advisor is obligated by law to act in your best interest. Advisors working under the suitability standard, on the other hand, only need to suggest products that are “suitable” for your condition, perhaps still more profitable for them than you.

Fiduciary duty provides stronger protection, particularly in tricky financial choices. Always ask:

- Are you a fiduciary 100% of the time?

- Would you be willing to sign that in writing?

- Do you ever get paid by third parties for products that you recommend?

You can also check fiduciary status through credentials like CFP® or by contacting organizations such as NAPFA or the SEC advisor database.

Robo-Advisors vs Human Advisors vs Hybrid Models

Technology has transformed the financial advisory industry. The emergence of robo-advisors—computerized platforms that generate and manage portfolios through algorithms—has made financial advice more within reach. These are best for young investors or simple needs.

Robo-Advisors

- Cost-effective and easy to use

- Best for simple objectives such as retirement or saving

- Poor customization and human touch

Human Advisors

- Full-fledged planning, emotional guidance, and flexibility

- Best suited for complicated situations and shifting goals

- Increased fees and minimum assets

Hybrid Financial Advisors

- Blend automated investing with human advisor access

- Affordable with a personal touch

- Still might not offer full customization for sophisticated strategies

As robo-advisor assets continue to rise and 60% of advisors consider using AI products to augment services, the future is in hybrid models. Based on your technology comfort level and complexity of requirements, each serves a different purpose.

How to Pick the Finest Financial Advisor for Your Requirements

There are thousands of professionals out there, and with that in mind, understanding how to find a financial advisor who aligns with your goals, values, and budget can be overwhelming. Finding a local financial advisor or digging online, it becomes less daunting when you begin with clarity and wit, with the right tools.

Getting the right advisor is not about searching for “financial advisor near me” on a search engine. It’s more about matching your financial requirement with an advisor’s area of expertise, fee methodology, and style of working. In this segment, we will walk you through a step-by-step approach, starting from determining your goals to searching for credible directories and posing the correct questions during your quest.

Define Your Financial Goals and Needs First

Before you contact an advisor, ensure you at least understand what it is that you need help with. When you are aware of your planning goals, it becomes easy to filter the professionals who are suitable for your case. Ask yourself:

- Are your goals long-term (retirement, legacy planning) or short-term (saving up to purchase a home)?

- Do you need simply investment management or complete planning, which includes taxes, insurance, and estate strategy?

- Are you on your own, self-employed, or an employee with wildly different tax and business planning needs?

- Are you just starting, are you in your earning years amassing your wealth, or are you in your retirement years, safeguarding what you have?

- How much can you afford to pay for guidance, or how much would you like to pay?

Establishing expectations enables you to select an advisor offering the proper amount of assistance at a proper fee.

Make use of Trusted Professional Directories and Networks

Instead of using ads or search engines, seek out vetted financial advisor databases. These sites guarantee that listed professionals adhere to particular requirements and qualifications. Large organizations are:

- NAPFA (National Association of Personal Financial Advisors): Fee-only fiduciaries with transparency

- CFP Board Center for Financial Planning: Certified Financial Planners searchable by specialty and location

- XY Planning Network: Suitable for Gen X and Y professionals, with advice that has no asset minimums

- Fee-Only Network: A focus on solo, commission-free advisors

- Financial Planning Association (FPA): Provides national listings with credential filters

California, New York, and Texas currently have the most advisors, but online services eliminate some of the limitations of location. Use search filters to limit your results by specialties, services, and fee models.

Referrals and Online Research Strategies

Another worthwhile strategy is requesting financial advisor recommendations from other professionals you already have confidence in—your CPA, estate lawyer, or even your banker. Friends or relatives can make some recommendations, too, but be certain to inquire:

- What exactly did the advisor do for you?

- How long have you been with them?

- What do you like (or dislike) about their style?

For added due diligence, do some online investigation of financial planners. Check their website, their LinkedIn page, and reviews at sites such as Yelp or Google—but note that not all reviews are authentic. Search for red flags such as ambiguous fees, over-the-top claims, or no licensing.

A robust web presence, along with good credentials, can indicate professionalism, but nothing takes the place of extensive personal screening.

What to Search for When Selecting a Financial Planner

Communication style and credentials in terms of how to choose a financial advisor are as important as services and fees. The right kind of planner not only becomes familiar with the technical details of the planning process but also builds trust, openness, and acceptance into the long-term visioning with your plans.

Communication style and credentials in terms of how to choose a financial advisor are as important as services and fees. The right kind of planner not only becomes familiar with the technical details of the planning process but also builds trust, openness, and acceptance into the long-term visioning with your plans.

In order not to lose the sense of purpose and make an informed decision, these are the factors that you need to keep in mind regarding a financial advisor: the real qualifications, area of expertise, and the style of service, just to name a few.

Minimum Credentials and Certifications

First, verify whether or not an advisor possesses professional designations. These financial advisor credentials indicate the degree of training, ethics, and specialty that an advisor has obtained.

| Credential | Focus Area | Requirements | Ideal For |

| CFP® | Comprehensive planning | Bachelor’s degree, financial coursework, 6,000 hours of experience, ethics exam | Individuals who want overall financial planning |

| CFA | Investment management | Graduate-level investment analysis, 3 exams, 4 years of experience | Investors requiring portfolio strategy knowledge |

| CPA-PFS | Tax + personal finance | CPA license + PFS designation, tax-oriented financial planning | High-income earners requiring tax optimization |

| ChFC | Advanced financial planning | 9-course curriculum frequently overlaps with CFP® requirements | Complex family or business planning situations |

As of 2024, there are over 97,000 CFP professionals in the United States, and increasing numbers of advisors are acquiring multiple credentials to represent more extensive knowledge. You can check certifications using:

- CFP Board’s official verification service

- FINRA’s BrokerCheck

- The SEC’s Investment Adviser Public Disclosure (IAPD) database

Credentials do count, particularly when considering advisors’ depth of knowledge and fiduciary responsibility.

Experience with Your Specific Situation

Above designations, the ideal advisor is one familiar with individuals like you. Search for a financial advisor specialization in your area. Simple or complicated, niche knowledge brings tangible value.

Look for advisors who have experience working with:

- Young professionals and student loans and budgeting

- High-net-worth individuals and estate or tax planning

- Business owners with succession plans and corporate benefits

- Retirees dealing with income drawdown and healthcare expenses

- Special situations like divorce, inheritance, or overseas assets

Praise direct questions such as:

“What kind of clients do you usually work with?”

“Do you have experience working with clients in circumstances like mine?”

Communication Style and Service Model

The quality of your advisor-client relationship often depends on communication. Don’t skip how your advisor communicates and interacts with you along the way.

Important considerations:

- Meeting style: Do you want to meet in person, via video conference, or by phone?

- Frequency of updates: Are performance reports monthly, quarterly, or on request?

- Responsiveness: How quickly do they respond to questions or concerns?

- Education and transparency: Do they explain concepts clearly or overwhelm you with jargon?

- Technology access: Is there a secure client portal or mobile app for real-time tracking?

An advisor’s communication style should suit your tastes and reinforce long-term confidence in your financial choices.

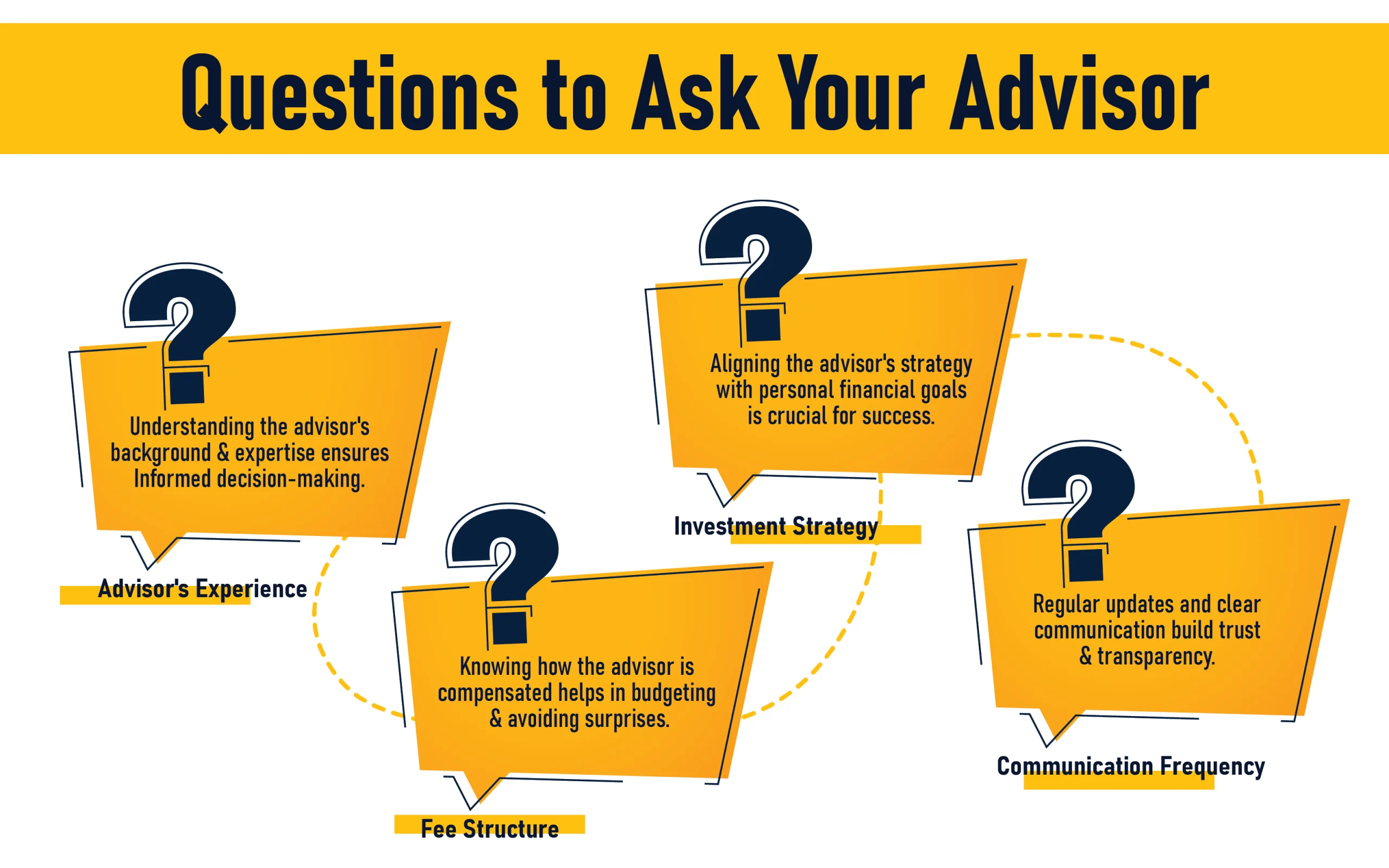

Essential Questions to Ask Prospective Financial Advisors

Before committing to a professional relationship, vetting your advisor is important. A set of smart financial advisor interview questions can guide you in finding out red flags, learning about their values, and whether they are suitable for your financial journey or not. This section offers an interview checklist of intelligent financial advisor questions—categor, categorized into the most essential areas: fees, fiduciary duty, and service philosophy.

Before committing to a professional relationship, vetting your advisor is important. A set of smart financial advisor interview questions can guide you in finding out red flags, learning about their values, and whether they are suitable for your financial journey or not. This section offers an interview checklist of intelligent financial advisor questions—categor, categorized into the most essential areas: fees, fiduciary duty, and service philosophy.

Compensation and Fee Structure Questions

Learning how financial advisor fees work is important for budgeting and transparency. Regardless of whether you’re paying a percentage of assets under management, a flat fee, hourly, or commission-based fees, always request hard numbers. Here’s what to ask:

- How specifically are you paid?

- What is your overall yearly fee for someone like me?

- Do you get commissions or other compensation based on selling products?

- Are there any extra fees I should anticipate?

Clarifying upfront how much a financial advisor charges avoids the shock later on and makes you less likely to overpay for standard services.

Fiduciary Duty and Conflicts of Interest

The legal requirements of a financial advisor can have a big impact on the quality of guidance you get. Ask straight fiduciary duty questions to make sure your advisor is devoted to your interests, not theirs.

- Are you a fiduciary 100% of the time?

- Do you have any conflicts of interest I should know about?

- How do you handle situations where your interests might conflict with mine?

The best advisors won’t hesitate to answer these questions—and may even provide them in writing.

Services, Investment Philosophy, and Track Record

Every advisor has their approach to wealth management. To determine whether their process aligns with your expectations, ask about their financial advisor services and decision-making style.

- What are the specific services you offer? (e.g., tax planning, estate planning, investment management)

- What is your investment philosophy and strategy? (e.g., passive vs. active management)

- Can you supply client references with situations similar to mine?

- How do you quantify and communicate performance?

- What if I’m not happy with your services?

Knowing their investment philosophy and service limits can make you more comfortable with the long-term value they deliver.

Red Flags and Mistakes to Steer Clear Of

Even the best advisor can fail if their motives—or qualifications—aren’t a good fit for your requirements. Most individuals make expensive errors employing a financial advisor purely due to the fact that they failed to detect the red flags in the early stages. Regardless of whether you are interviewing applicants or second-guessing someone already on your payroll, an understanding of the most significant financial advisor red flags can guard your money and sanity.

Even the best advisor can fail if their motives—or qualifications—aren’t a good fit for your requirements. Most individuals make expensive errors employing a financial advisor purely due to the fact that they failed to detect the red flags in the early stages. Regardless of whether you are interviewing applicants or second-guessing someone already on your payroll, an understanding of the most significant financial advisor red flags can guard your money and sanity.

Fee Structure Red Flags

Transparency is essential regarding how an advisor gets paid. Certain red flags can signal possible conflicts of interest or excessive fees:

- Hidden or unclear fees in fine print or bundled products

- Higher-than-needed fees for simple services that do not suit your requirements

- Being pushed to invest in high-commission products, including annuities or insurance packages

- Failure of fee transparency when requested for a detailed breakdown

If an advisor cannot explain their compensation clearly, or is ot keen to do so in writing, that’s a red flag to leave them.

Behavioral and Professional Red Flags

The way an advisor acts may inform you as much as their qualifications. Listen to your intuition if you witness:

- Pushy sales efforts that drive urgency at the expense of thoughtfulness

- Guarantees of guaranteed returns—a huge red flag in a market-based world

- Lack of licenses or credentials, or their inability to be confirmed online

- Inadequate communication, such as delays, cryptic updates, or no-shows

- Continued hype about certain products or approaches without clearly outlining them

The correct advisor will steer—not push—you toward decisions in your best interest.

Due Diligence Mistakes

Even the most intelligent clients sometimes miss the background checks. These financial advisor background check errors can lead to the wrong hire:

- Failure to check the advisor’s record on FINRA’s BrokerCheck or the SEC IAPD

- Missing reference checks with current or former clients

- Selecting an advisor on likability rather than experience or qualifications

- Not comprehending the entire fee structure

- Assuming credentials without verification

Doing your homework upfront can prevent serious regrets down the road.

The Best Ways to Collaborate with Your Financial Advisor

The real value of an advisor doesn’t come from a single meeting—it’s built over time through a collaborative, transparent advisor-client relationship. Once you’ve selected a professional, working with a financial advisor effectively means staying engaged, setting clear expectations, and revisiting your goals as life evolves.

The real value of an advisor doesn’t come from a single meeting—it’s built over time through a collaborative, transparent advisor-client relationship. Once you’ve selected a professional, working with a financial advisor effectively means staying engaged, setting clear expectations, and revisiting your goals as life evolves.

Solid partnerships are founded on joint responsibility. Your advisor needs to serve as a guide, but so do you, in establishing what success means and how you will be held accountable through quantifiable results. Here’s how to develop a long-term relationship that evolves with your financial needs.

Setting Clear Expectations and Benchmarks

Begin by defining precisely what you wish to accomplish with your advisor. Early retirement, preserving wealth, or paying for your child’s education, setting specific success metrics, defines the tone of the relationship.

Resolve:

- How and when you prefer to communicate (in-person, remote, email, phone)

- Frequency of meetings and how progress updates will be communicated

- Performance targets, i.e., returns on the portfolio with risk tolerance

- A time frame to review progress and reassess goals

Talking about expectations ahead of time decreases misunderstandings and keeps you both on the same page.

Regular Evaluation and When to Think About Changing

Similar to any service provider, a financial advisor should be reviewed from time to time. Annual performance evaluations are a great time to review your plan, revise your goals, and make sure the strategy continues to fit.

You might have to re-evaluate, too, if:

- Your circumstances change (e.g., wedding, inheritance, or retirement)

- For new goals, your advisor lacks the necessary experience.

- You see deteriorating service quality, bad communication, or failing performance objectives

If you’re reviewing your financial advisor and see recurring issues, don’t be afraid to look elsewhere. When considering when to change advisors, be sure to:

- Ask for a transition plan for your financial records

- Know any fees or limitations

- Select a new advisor before ending the current relationship

A good advisory relationship must change with your life, not keep you stuck.

Conclusion: Take Control of Your Financial Future

For your long-term financial well-being, hiring a financial advisor is one of the most crucial choices you will ever make. Not to mention credentials and experience considerations, service models and fee evaluations are part of the process that cannot be disregarded. There is no need to hurry, ask the right questions, and have the highest priority of transparency and fiduciary duty.

The most outstanding advisors are not just salespeople of the products, but your co-workers in the field of money. If you are saving towards retirement, conceptualizing your wealth, or experiencing a life change that is important to you, choosing the right financial advisor can be fraught with confusion, insecurity, and nervousness.

Start searching now. You take charge of your future, then have the support of a trained advisor who will take an interest in you, every step of the way.